Businesses are now actively filing their GSTR-1 returns after completing the GSTR-3B returns for the previous month. Proper reconciliation between these forms is critical to ensure accurate reporting and avoid any compliance issues.

Here is a detailed guide on matching GSTR-3B with GSTR-1 and GSTR-2:

Understanding GSTR-3B, GSTR-1, and GSTR-2

- GSTR-3B:

A summary-level interim return where businesses declare consolidated tax liability and eligible Input Tax Credit (ITC). It is designed for quicker compliance. - GSTR-1:

A detailed return that captures invoice-wise and rate-wise details of outward supplies. - GSTR-2:

A return for inward supplies, capturing the details of ITC claimed and tax liability on inward supplies under reverse charge.

Why is Matching Important?

The summary reported in GSTR-3B must align with the invoice-level details reported in GSTR-1 and GSTR-2 to ensure consistency in tax filings. Accurate matching ensures:

- Compliance: Prevents notices from tax authorities.

- Transparency: Minimizes discrepancies in ITC claims and tax payments.

- Seamless Process: Reduces errors while filing GSTR-3.

Steps to Match GSTR-3B with GSTR-1 and GSTR-2

- Outward Supplies:

- Verify that the summary of outward supplies in GSTR-3B matches the invoice-wise details in GSTR-1.

- Exclude inward supplies liable for reverse charge while reconciling outward supplies.

- Input Tax Credit (ITC):

- Compare ITC details in GSTR-3B with those in GSTR-2.

- Ensure that the ITC claimed aligns with the tax liability reported for inward supplies under reverse charge.

- System-Populated Data in GSTR-3:

- Use the system-generated figures in GSTR-3 based on GSTR-1 and GSTR-2 to cross-check your reported data.

- Verify if the tax paid through the Electronic Cash Ledger and Electronic Credit Ledger while filing GSTR-3B is accurately captured.

- Handling Differences:

- If there are no discrepancies between the output tax liability and eligible ITC in GSTR-3B and the details in GSTR-1 and GSTR-2, proceed to submit GSTR-3 without additional tax payments.

- In case of differences, reconcile the data and pay any additional tax liability before final submission

Revised Deadlines

To ease compliance, the GST Council extended the filing deadlines for GSTR-1, GSTR-2, and GSTR-3 for the month of July. The extended deadlines offer much-needed relief to businesses, ensuring ample time for reconciliation and accurate filing.

Key Takeaways

- GSTR-3B serves as a bridge for interim compliance, but it must match with the detailed returns (GSTR-1 and GSTR-2).

- Regular reconciliation and validation of data reduce errors and ensure smooth GST filing.

- Businesses should utilize system-generated tools and reports for efficient reconciliation and filing.

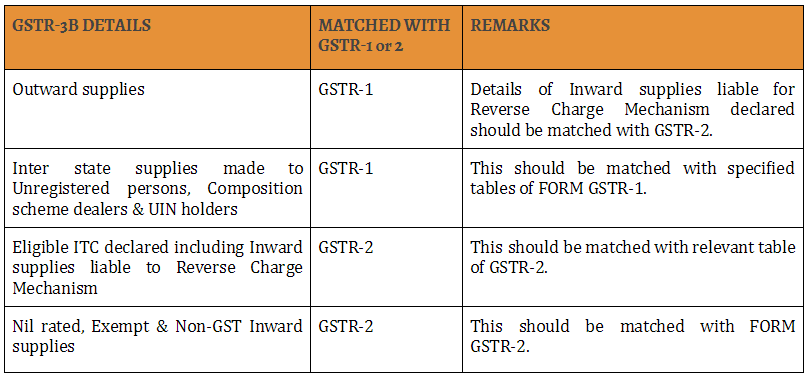

The details of matching of GSTR-3B with GSTR-1 & GSTR-2 are shown below:

Accurate matching of GSTR-3B with GSTR-1 and GSTR-2 is essential for seamless GST compliance. Businesses must adhere to timelines and maintain thorough documentation to avoid any discrepancies or penalties.